Why AI tool selection has quietly become a strategic architecture decision — and how to make it.

Most companies think they have an AI tool problem

They do not. They have an ecosystem problem.

Over the last two years, most organisations walked into AI through whichever door opened first — ChatGPT for one team, Microsoft Copilot for another, Claude for the writers, Gemini for the Google-native departments, Perplexity for research, plus the AI now built into Salesforce, HubSpot and SAP. The result is predictable. Marketing standardised on one tool, finance experimented with another, sales lives inside CRM-native AI, leadership bought ChatGPT Enterprise, and the developers picked Claude Code or Cursor.

The company now holds five or more AI subscriptions with overlapping capabilities, inconsistent governance, duplicated cost and no clear owner. That is where a large share of mid-size companies sit today: excited, experimenting, and increasingly unsure which AI stack they should actually commit to. Beneath the noise, though, something more important is happening. The market is starting to converge.

The first AI wave was about the model. The second is about the stack.

The opening phase of AI competition was almost entirely about the model itself — who had the smartest reasoning, the best writing, the strongest benchmark scores, the largest context window. That race produced extraordinary innovation. It also produced confusion for anyone trying to build a long-term operational strategy, because most organisations do not actually buy models. They buy ecosystems. And those ecosystems are starting to overlap.

Microsoft builds on OpenAI. Perplexity runs frontier models — including Claude — underneath its interface. Cursor switches between models dynamically. Browsers now embed AI natively, CRM platforms ship their own assistants, and ERP systems are becoming AI-native operating layers. Meanwhile, open standards such as the Model Context Protocol (MCP) make it steadily easier for AI systems to connect across tools and workflows.

The effect is that the underlying model is becoming abstracted away. Users increasingly care less about which frontier model sits beneath the surface and more about where AI lives, what it connects to, how it fits existing workflows, whether governance exists, and whether teams actually adopt it. The AI contest is no longer only about intelligence. It has become a contest for operational gravity.

Operational gravity decides the winners — quietly

Most executives still ask: “Which AI tool is best?” The more useful question is: “Where does our company already live?”

If an organisation runs on Word, Excel, Outlook, Teams and PowerPoint, Microsoft Copilot holds an enormous natural advantage — not necessarily because the model is superior, but because the workflow friction is lower. The same logic favours Gemini in Google Workspace companies, Agentforce in Salesforce-heavy organisations, and HubSpot’s Breeze for marketing and sales teams already centred there.

This is one of the biggest misconceptions in the AI market right now. Companies assume they are choosing a chatbot. They are choosing an operating layer. That distinction matters far more than any benchmark chart. The plumbing matters less than where you live and work.

AI no longer lives in one window

Most organisations still picture AI as a chat box — a window, a prompt, a response. But AI now operates across four distinct surfaces, and the strategic conversation changes once you see them clearly.

Chat tools help teams write, summarise, analyse and think.

Desktop and cowork agents execute multi-step tasks, manipulate files and run asynchronously.

Browser agents research, compare vendors and complete repetitive web tasks.

Coding agents build, refactor, debug and automate engineering work.

These surfaces increasingly connect into one another. The line between browser, operating system, coworker, assistant and workflow engine is dissolving. The future AI stack is not one application — it is a layered operational environment.

There is also a fifth surface, and it separates companies experimenting with AI from companies operating on it: the API layer. The first four are bought as seats. The API layer is not — and that is the point. It makes retrieval-augmented generation (RAG) possible on a company’s own data, so models answer from its contracts, records and source code, which consumer chat cannot safely touch. It enables agentic workflows with real authority — agents that hold credentials, edit ERP records and route tickets under the company’s audit and control — and custom, fine-tuned models for medical, legal or technical domains. It also changes the economics: per-token pricing, with automation routed through platforms like n8n, is often far cheaper than per-seat licensing at scale.

The API layer is not a more technical version of the same product. It is a different relationship with AI — one where the organisation, not the vendor, sets the terms. And the first thing that relationship changes is who controls the data.

In Europe, the stack decision is also a governance decision

For European companies, and German ones in particular, AI selection is no longer only a productivity question. It is simultaneously a governance, architecture, compliance and sovereignty decision. This is where AI conversations become dangerously oversimplified. Consumer AI tools feel interchangeable on the surface; underneath, they are not. Data residency, retention policies, audit logging, deployment models, training defaults and tenant isolation vary significantly between vendors and plans.

That difference matters far more once AI moves beyond experimentation and into operational workflows — because eventually AI stops helping employees draft emails and starts touching customer records, financial forecasts, HR systems, contracts, procurement and strategic planning. At that point AI becomes infrastructure, and infrastructure decisions are governance decisions.

This is why enterprise adoption in Europe increasingly happens through Azure OpenAI, AWS Bedrock, Google Vertex AI, private-cloud tenants and EU-hosted environments rather than consumer chat subscriptions alone. European organisations want the productivity of frontier AI without losing control of where data lives, whether models train on it, who can access it and how AI actions are governed. Once AI agents gain operational authority — accessing ERP systems, updating CRM records, routing approvals — GDPR and governance stop being side conversations. They become part of AI strategy itself.

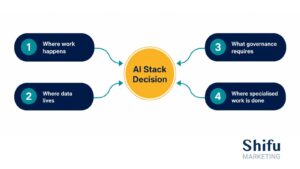

The Operational Gravity Test

Before comparing vendors, answer four questions. Together they reveal where your company’s operational gravity already pulls — and that pull, more than any benchmark, should anchor the stack decision.

- Where does the daily work already happen? The productivity suite your teams open every morning (Microsoft 365, Google Workspace) is the strongest gravitational source.

- Where does the critical business data already live? The CRM and ERP that hold customer and financial records pull the agent layer toward their native AI (Agentforce, Breeze, SAP Joule).

- What does governance require? Data residency, audit and training-default rules may override convenience and push the stack toward a private-cloud or EU-hosted deployment.

- Where is specialised work done? Engineering, research and strategic writing often justify a second, specialised layer (a coding agent, a research tool, a strategic-writing model) regardless of the primary ecosystem.

HOW TO USE IT Score each question for pull strength. A company with strong answers to 1 and 2 in the same ecosystem has a clear primary stack. Strong, conflicting answers signal a deliberate hybrid — see the next section. |

The future belongs to hybrid AI stacks

For most companies, the winning AI strategy will not be one vendor, one model, one interface. It will look more like one primary ecosystem, several specialised AI layers, shared governance, reusable organisational context and interoperable workflows.

A Microsoft-first organisation might run Copilot for everyday workflow, Claude for strategic writing, Perplexity for research, the AI inside its CRM and ERP, and APIs for automation and governance. A Google-centric company might build around Gemini, Workspace, Chrome’s AI and Vertex AI. More advanced organisations move beyond consumer subscriptions entirely — building private AI layers, workflow automation, RAG systems, custom copilots and model-independent orchestration. This is the point where AI stops being a tool and becomes infrastructure.

Why many companies are “waiting it out” — and why that is often rational

Executives feel trapped between urgency, confusion, FOMO, governance concerns and vendor lock-in fears. Every week brings new models, interfaces, agent frameworks and pricing structures. The result is decision fatigue. Many organisations are delaying major commitments — not because they doubt AI, but because they fear choosing the wrong architecture too early.

That caution has a basis. On April 22, 2026, OpenAI, Google and Salesforce all announced enterprise AI agents within hours of each other — a single day that captured how fast the ground is still moving. Models commoditise quickly, interfaces converge, ecosystems overlap, APIs standardise capabilities and open-weight models keep improving. The market is not stabilising yet. It is converging. Choosing an AI stack has come to resemble choosing an operating system for the company itself — so some hesitation is strategic, not resistant.

The meta-skill is becoming more valuable than the tool

Here is the most important shift. The durable advantage is no longer the tool. It is the organisational context built around it.

Prompts, workflows, brand voice, governance structures, AI-enabled processes and operational memory increasingly transfer across vendors. Tools may change, models may change, interfaces may change — but organisational AI maturity compounds. The companies that win will not be the ones chasing every new release. They will be the ones that reduce fragmentation, operationalise AI responsibly, create reusable workflows, integrate AI into operations and balance flexibility with governance.

That is the next phase of enterprise AI. Not chatbot experimentation — operational convergence. The race may not be won at the model layer at all. It is increasingly won at the workflow layer. And that changes how companies should think about AI entirely.

SUMMARY AI stack selection has shifted from a model comparison to an architecture decision. The right primary ecosystem — Microsoft, Google, OpenAI, Salesforce or another — is the one closest to a company’s existing operational gravity: where work happens and where data lives. Most companies will run a hybrid: one primary ecosystem plus specialised layers, unified by shared governance. Shifu Marketing recommends starting with the Operational Gravity Test before any vendor comparison. |

Book an AI Strategy Workshop — a half-day leadership session to map your operational gravity and decide the AI stack that matters most for your company.